in UK, rainy day fund, 4 to 6 months of your absolutely fixed outgoings, for me that's around £25k pbly. remaining depends on time horizon and your credit. if you have a long time horizon and good credit id put the rest in an investment BTL property, incorporated, however you will have to wait for a good deal which isnt available immediately. assuming you expect to land a deal in ~ 3 to 6 months id put it in easy access savings which will give you about 4% return, if you expect to wait for longer, like a year, then id put half the money in an index tracker for stock markets, and other half in fixed term deposit.

so with numbers assuming you get a good deal in six months

75k -> 76.5k

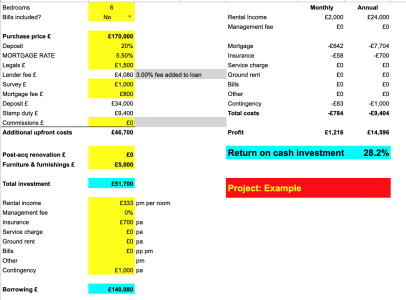

you find a rental property, ~£300k value yielding ~6.5%, gross rental of 19.5k, but buy it at a 10% discount so 270k, 20k purchase cost and tax.

mortgage of 215k, at 5.5% ~£12,000 interest cost.

10% cash on cash yield, assuming it appreciates by twenty percent in value over 5 years, your total return is 60k+37.5k ~100k on 75k investment over 5.5 years, which is equivalent to ~16.6% annual returns assuming rents dont increase and ur maintenance costs are neglegible.

)")